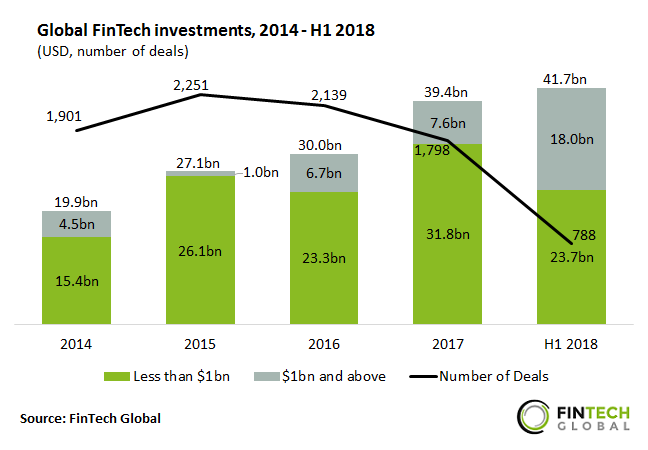

The global Fintech sector raised $41.7bn in the first half of 2018, surpassing last year’s record total

- Global FinTech investments increased steadily between 2014 and 2017 from $19.9bn to $39.4bn at a CAGR of 18.5%. This trend accelerated in the first half of 2018 when $41.7bn was invested across 789 deals.

- There were two megadeals valued above $1bn in the first half of the year including a mammoth $14bn investment in Ant Financial, the payments affiliate of China’s Alibaba Group. The Series C round was led by Temasek Holdings and GIC with co-investment from Sequoia Capital and Warburg Pincus, among others. This single deal accounted for a third of the total capital raised during H1.

- Deal activity peaked in 2015 at 2,251 deals, and has been declining since. This downtrend is set to continue in 2018, with the 789 deals completed equating to just 43.9% of last year’s total.

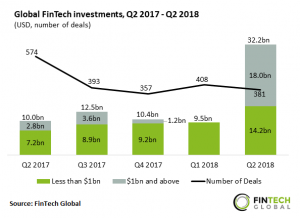

Investments skyrocketed in Q2 to set a new quarterly funding record

- Capital raised in Q2 2018 surged to reach a record of $32.2bn. This represents an increase of 3.2x compared to the same quarter last year.

- Even when the two megadeals valued over $1bn are disregarded, Q2 2018 still remains the strongest funding quarter to date.

- Despite the high funding total, deal activity was historically low at just 381 deals. This is the second lowest value recorded between 2014 and Q2 2018.

- This resulted in the average deal size, excluding megadeals, jumping from $26.5m in Q1 2018 to $41.5m in Q2.

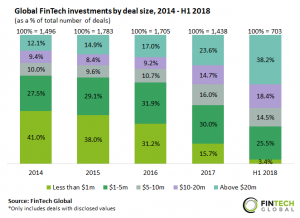

The global Fintech industry is maturing rapidly

- There was a significant shift towards larger investments between 2014 and 2017. Deals valued below $1m decreased in share from 41% to 15.7% over this period. This trend continued in H1 2018 when just 3.4% of all deals were in the sub-$1m category.

- Conversely, deals valued above $20m increased in share from 12.1% in 2014 to 23.6% in 2017. In the first half of 2018, this figure jumped to 38.3%.

- This pattern of fewer, larger deals indicates that the global FinTech market is maturing at a fast pace.

- Notably, the Marketplace Lending sector has the lowest proportion of deals valued less than $1m at 20.4%. It also has the highest proportion of large deals, with a third of all investments in the sector valued above $20m.

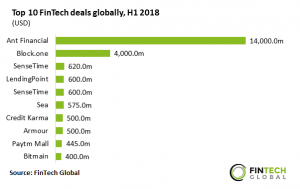

The top 10 Fintech deals in H1 raised almost $22bn

- The aggregate of the top 10 FinTech deals in the first half of 2018 is $21.8bn which equates to 52.3% the total capital raised during this period.

- The largest deal in H1 2018 was the previously mentioned $14bn investment in Ant Financial. This was followed by a $4bn funding round raised by Block.one, an end-to-end blockchain solutions provider, in the largest initial coin offering (ICO) to date.

- SenseTime, a Beijing-based provider of facial recognition technology, features twice in the top 10. The company initially raised $600m in a Series C round led by Alibaba Group. This was followed by a further $620 in Series C+ funding, led by Tiger Global Management, Silver Lake Partners, Fidelity International and HOPU. The funding will be used towards research and development, as well as hiring talented researchers.

The data for this research was taken from the FinTech Global database. More in-depth data and analytics on investments and companies across all FinTech sectors and regions around the world are available to subscribers of FinTech Global. ©2018 FinTech Global